Cash flow, where your money goes as its coming in, isn’t the sexiest part of planning. Asset allocation and tax reduction strategies typically are the highlights of financial advice.

Think of your cash flow is the oil in the engine powering you towards the future. No matter your goals if you aren’t putting cash in the right places you can’t reach them. After cash flow is handled, you can get into the weeds with optimizing the other parts of your financial life.

I am a big fan of setting goals for each account. This way we can mark it “done” and that money can instead flow into another account.

Additionally, I like to use monthly income multiples instead of monthly expense multiples. It helps keep the math simpler and naturally builds in extra padding in these accounts.

So Where To Put Cash?

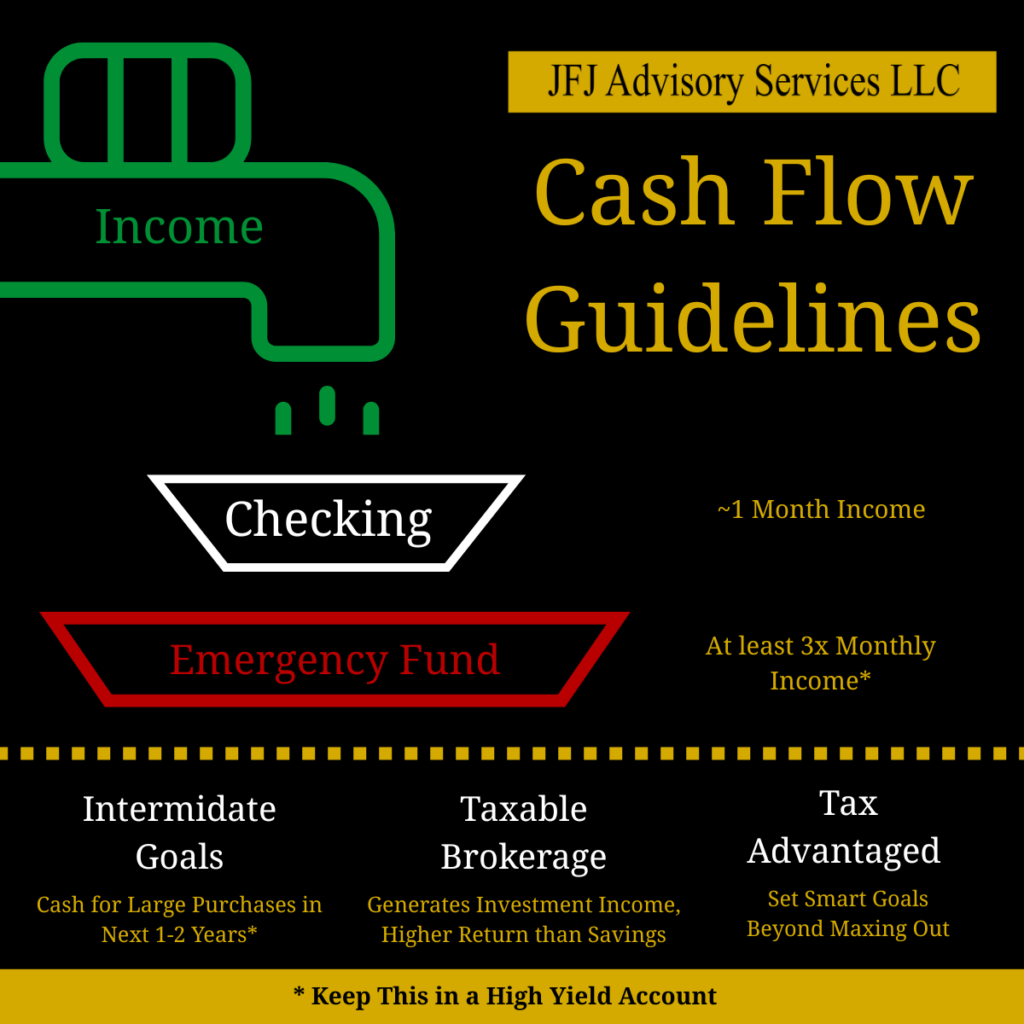

I believe cash should be going into one of five places:

- Checking

- Emergency Fund

- Intermediate goals

- Taxable Brokerage

- Tax Advantaged Accounts

Checking

Likely your smallest account. ~1 month worth of income here, just to cover your expenses. All while having a little wiggle room.

I usually don’t raise concerns about your budget, unless a) you request my input, or b) it’s a large enough issue I wouldn’t be serving you properly if I didn’t. I am mostly in the business of helping clients do more with the cash they’re not spending.

Emergency Fund

How much we keep here depends on several factors including income variability and risk tolerance. Three months of income is usually the minimum I suggest. It can go higher from there if, for example, a majority of your income comes from commissions, or you’re concerned about layoffs. However much you need to sleep soundly.

The first two accounts need to be handled first. It’s not recommended to start investing without establishing an emergency fund.

The order of next three will depend on your current goals and often you can put money towards 2 or 3 of them at simultaneously.

Intermediate Goals

Whether this is a new (to you at least) car, vacation, or a down payment on real estate. This account is used to save money for goals you want to achieve in the next 1-2 years.

Often these are goals that can worked towards alongside contributing to investment accounts.

If you’re saving for an Alaskan cruise and have 30 years until retirement, we could focus on the vacation. Putting a large amount towards the cruise and making small contribution towards retirement, knowing compound growth will do most of the work.

For your emergency fund and intermediate goals you better make sure you’re getting a competitive yield on your cash.

I offer Flourish Cash to ensure clients (or anyone interested) are getting high yield, FDIC insurance, and same-day transfers without any fees.

Taxable Brokerage

For many of my clients this can often be the most popular destination for cash. No contribution limits, no required distributions, wider selection of investment strategies, and no penalties on withdrawals ever.

This account offers maximum flexibility. Growth, income, preservation, whatever you like.

If you decide to start a business in 10 years you have the money. If you don’t need to tap into it, you can leave a legacy. If you want to start living off your investments before 65, you need to be able to access them before 65.

Tax-Advantaged Accounts

Maxing these out each year may not always be the best strategy. I don’t intend this to come across as a hot take or engagement bait.

For IRAs a lot of my clients want financial freedom before 59.5. In this case they need more flexibility from their investments. 401(k) with match is a slightly different story.

For 529s it would be good to at least consider using a mixture of funding options to pay for your child’s education.

These accounts DO have purposes. Planning for these accounts may be the most math-intensive calculations I do. Finding the sweet spot between overfunding (money could be put to use elsewhere for greater effect) and underfunding (missing or having to delay your goal) is a challenge. A challenge I enjoy tackling.

Do You Have a Plan for Your Cash Flow?

Before you worry about asset allocation, tax optimization, or if you have enough insurance, you have to make sure you know where you money is going. Organizing your cash flow can provide clarity and a sense of security to your financial picture.

Have questions about your cash flow? Book some time to talk

This information is provided for informational purposes only. Not intended as a recommendation. Please do your own research or schedule time to speak with us about your specific situation. All investing involves risk, including the risk of loss.

For more information and to read our disclosures visit adviserinfo.sec.gov

JFJ Advisory Services LLC CRD# 322407

JFJ Advisory Services cannot guarantee the outcome of any investment plan.